Wait, how did hailey sell so fast?!

and hurry up and tell me who's next!! 🔮...

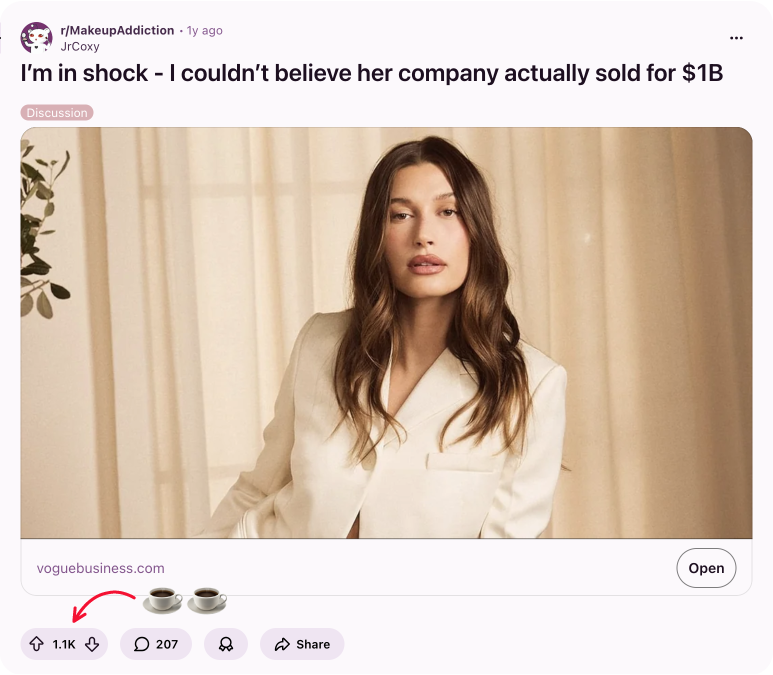

Yeah we all know Hailey Bieber sold rhode to e.l.f. Beauty for up to a sweet $1B in 2025, just 3 years after launch. That’s old news at this point. But there was this wild Reddit thread calling BS on the whole thing. It had 207 comments, 1.1K upvotes, and was about half right. I made it my distraction from real work mission to find the other half.

here’s what i’m overthinking

That “Mean Girl-y” Reddit thread

The 6 decisions that made rhode worth $1B

Who else wants to be a billionaire

The playbook you need to steal from rhode

⏲️ Read time: 15 minutes. Get cozy, you’re in for a wild ride.

I was doing what I do on a slow Sunday afternoon, which is soft-stalking Reddit communities I have no business being in, when I found a thread in r/MakeupAddiction that made me do the wide-eyed emoji face. The post title read, “I’m in shock — I couldn’t believe her company actually sold for $1B.”

Soooo shady! I’m in…

The thread was ten months old, the OP had 1.1K upvotes, and the comments were full of side-eyed golf claps, which in beauty Reddit terms is the equivalent of thousands of Regina George’s telling Hailey they liked her skirt.

IYKYK.

The comments were also exactly what you’d expect from a community of people who care deeply about whether a lip treatment is worth $16.

Absolutely nobody in there was buying that Hailey did any of the work to build rhode, and they even had me looking side eyed at old girl at one point. One person who claimed to have done a grad school case study on L’Oréal declared “there is no way” and noted that the speculation about Hailey Bieber being broke was “looking true.”

Someone else pointed out that Justin Bieber sold his entire music catalogue for $220 million, and that $600 million in cash up front was “still wild” by comparison, which is actually one of the more useful pieces of financial context I’ve ever encountered in a Reddit thread.

These skeptics were using their full chests in this thread. The general vibe was: rhode is “soooo mid,” no celebrity brand is worth that, and the whole thing felt like a light flex from e.l.f., who just wanted to spend money. Ay dios mio!

And then it got just a little bit more interesting.

Someone surfaced what I can only describe as the most delicious subplot in the entire thread: the suggestion that the brand’s negative reviews and D-rated BBB score might not have been entirely organic, and that Selena Gomez’s fanbase (a group with a well-documented history of organized militia-esque online behavior) had potentially been running a coordinated rhode review-sabotage campaign!

Nobody confirmed this and nobody denied it. It’s still unconfirmed and I choose to believe it anyway.

But I digress...

By the time I’d scrolled far enough to reach the comment chain that had somehow drifted into a person describing the panic attack they had after receiving a $15,000 tip (involving an escort, a client from China who didn’t know dinosaurs were real, a copy of Jurassic Park, a bag of cash), I finally struck some gold.

Buried about two-thirds of the way down, someone introduced a theory about domestic manufacturing facilities and tariff exposure that was significantly more financially sophisticated than anything else in the thread (we’ll come back to that shortly).

how did everybody miss this?

The 207-comment thread managed to be both completely right and completely wrong at the same time, which is basically Reddit’s whole thing.

But for all the theories and passive-aggressive jabs thrown at Hailey Bieber the person, the thread missed the actual interesting question. Forget whether rhode deserved $1B. If Hailey pulled this off in 35 months, who’s sitting in a warehouse somewhere right now building the exact same thing?

And look, I’ll admit that the sale timing and amount was outrageous by any standard. But rhode didn't happen by accident, no matter how much Reddit wants to believe it did. There were six decisions Hailey and her team made that turned a celebrity skincare line into a billion-dollar acquisition in 35 months, and they're all visible from the outside if you know what to look for.

1. rhode’s three-product launch was everything

When rhode launched in June 2022, it had exactly three products, the Peptide Glazing Fluid ($29), the Barrier Restore Cream ($29), and the Peptide Lip Treatment ($16). Just three things. For a celebrity beauty launch, this is almost aggressively minimal.

Kylie Cosmetics launched in 2015 with 29 lip kits, and SKKN by Kim launched in 2021 with 9 SKUs on day one. Most celebrity beauty brands launch like a clearance event, dumping a wide assortment into the market and hoping something sticks.

Hailey put three things on a shelf, sat back, and let the customer tell her which one mattered.

The customer picked the Peptide Lip Treatment.

The more interesting thing about that launch wasn’t which product won. It was everything that rhode didn’t have on the website. With three products, every unit of manufacturing attention, every piece of marketing budget, and every operational decision was concentrated on exactly three SKUs. That’s it.

This matters more than it sounds, because if you are an acquirer doing due diligence, there is a real difference between a brand doing $100 million in revenue spread across 30 products and a brand doing $100 million coming from 3 hero SKUs.

The first one is a portfolio you have to rethink the day after the deal closes. The second one basically runs itself.

2. they basically spent zero on influencers

Most beauty brands spend somewhere between 15% and 25% of revenue on influencer marketing. rhode spent almost nothing in that category at launch, because Hailey Bieber was the only influencer the brand needed.

When e.l.f. ran the financials during due diligence, the customer acquisition cost would have looked borderline absurd compared to industry norms. An owned audience of that scale, with that level of brand identification, with no ongoing cost attached to it, is the kind of asset that doesn’t show up cleanly on a balance sheet but shows up very clearly in the margin profile.

e.l.f. wasn’t acquiring a brand with $15 to $20 million per year in influencer spend baked into its operating costs. They were acquiring a brand whose primary marketing channel was essentially free, forever, as long as Hailey kept posting.

That is a very different financial profile than it looks from the outside, and it’s a big part of how the margins came in at 40%.

3. the phone case was more than just a cute story

In September 2023, rhode launched the Pocket Case. It’s a pretty basic phone case, but with a slot built into the back to hold the Peptide Lip Treatment. So now the lip product literally lives on your phone, where you carry it around all day showing it to everyone you meet without realizing you’re doing free marketing for a beauty brand.

It sold out the day it dropped.

More than 700,000 cases sold at $38 each, which is around $26.6 million from a phone case. A phone case! For a skincare brand whose whole product line at the time was basically three things.

On the surface it looks like a sold-out accessory, but what you’re actually looking at is a customer base that’s loyal enough to follow the brand out of skincare and into something completely unrelated. That almost never happens with celebrity beauty brands. The customer is usually loyal to the celebrity, the brand underneath is paper-thin, and any product extension reads like a cash grab.

I think the Pocket Case was probably the biggest proof to e.l.f. that rhode was much more than that.

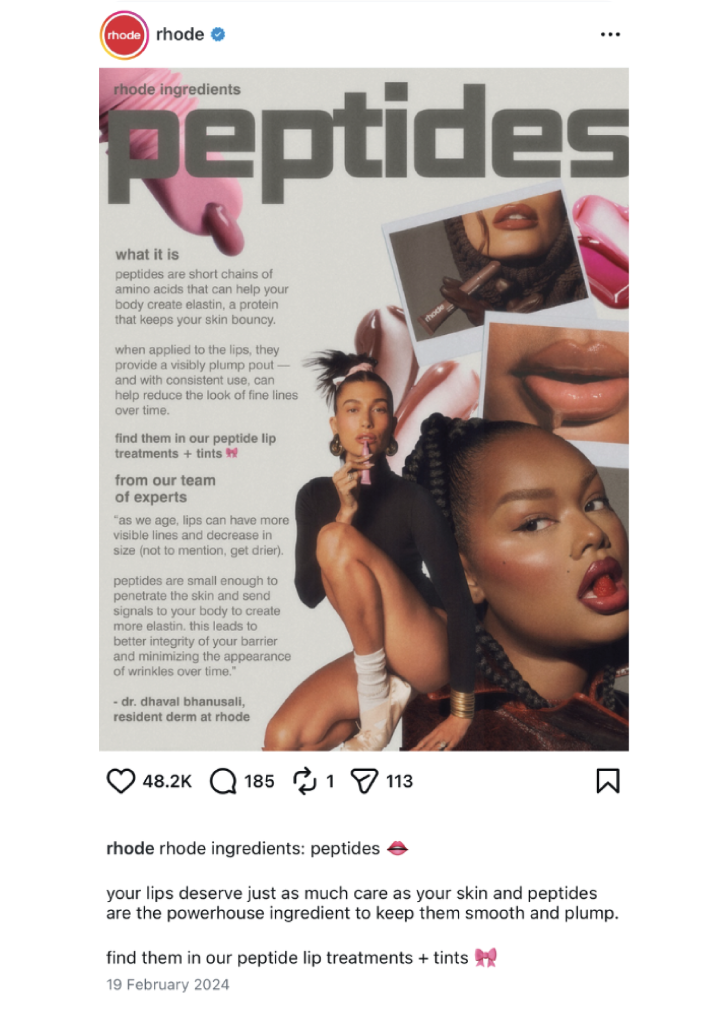

4. the formulations were actually legit

Most celebrity beauty brands are basically marketing businesses with some cosmetic products attached (I see you, Kylie girl). The formulations are usually generic, mass-produced stuff that any contract manufacturer can crank out, developed quickly and cheaply, and the whole thing relies on the founder's reach to move units.

rhode went a different direction and they worked with real cosmetic chemists. The Peptide Lip Treatment actually had peptides in it, in amounts that did something, and beauty editors who showed up ready to dismiss it as a vanity project ended up actually recommending it. That doesn’t happen with most celebrity beauty drops.

For e.l.f., this is the difference between buying a brand and buying a moment. Products that don’t work have a short shelf life once the launch energy fades and trolls bots customers start leaving honest reviews. JLo Beauty launched in 2021 with performance generally described as disappointing, and you can guess why. e.l.f. wasn’t worried about waking up to find rhode had collapsed the second Hailey’s engagement numbers dipped.

The ingredient choice was also not an accident. rhode launched in June 2022, which was right around the moment peptides were crossing from clinical dermatology into mainstream beauty conversation. Early enough to help shape the moment, before the Silicon Valley tech bro Peptide Panic in Needle Park spread through the Manosphere. By 2023, every brand from Neutrogena to niche Sephora indies had a peptide serum on shelf, but rhode had already owned the word.

“Glazed donut skin” gave customers the aspiration. Peptides gave them the ingredient story to justify the purchase. Most celebrity beauty brands give you one or the other. rhode gave you both, at $16, which is a much harder thing to pull off than the price tag suggests.

5. the name problem wasn’t a problem after all

This one is way too underappreciated. Hailey originally wanted to call her company rhode for a fashion brand, but the name was already in use by a clothing company co-founded by Purna Khatau and Phoebe Vickers (sidenote, read this article to learn more about that absolutely insane saga).

At the end of the day, legal reality confined rhode to beauty.

What sounds like an annoying setback in the origin story was actually one of the most important structural factors in the brand’s success, because it prevented the scope creep that kills most celebrity brands before they develop real depth.

The list of distractions available to someone with Hailey Bieber’s reach is essentially infinite (a fashion line, a fragrance, a home goods collab, a shoe drop, a hotel partnership, a rap album…smh). By being legally blocked from one of the most tempting distractions, she was forced to stay in a single category where she could build genuine credibility rather than spreading thin across seven.

Getting locked out of fashion was, accidentally, the best business decision rhode ever made. I’m guessing Hailey probably doesn’t lead with that in interviews.

6. the timing wasn’t an accident

e.l.f. Beauty’s stock had climbed roughly 80% in the year leading up to the acquisition, giving the company one of the highest valuation multiples in consumer goods and a very attractive acquisition currency.

The company had already bought Naturium in 2023 for $355 million and had both the appetite and the financial position to pay $1 billion for a 3-year-old brand. When Hailey accepted $200 million in e.l.f. stock as part of the deal, she was accepting shares priced near their peak.

Aaaand the stock came down after.

That same deal, structured six months later, looks materially different on paper. The market timing was equally deliberate.

Hailey was watching the celebrity beauty category the same way any rational founder watches a market before deciding to exit. She had watched Coty buy 51% of Kylie Cosmetics for $600 million in 2019 and write the investment down significantly by 2022.

She had watched SKKN by Kim get middling reviews and struggle to break through. The narrative around celebrity beauty was already turning, and the window for a 9-figure exit on a brand barely past its third birthday was not going to stay open indefinitely.

Hailey sold into enthusiasm rather than waiting to find out what the category looked like after the enthusiasm faded.

That’s six brilliant operational decisions.

A tight product launch, a founder who was her own only influencer, a phone case that proved loyalty could travel, formulations that held up under scrutiny, a name dispute that accidentally prevented brand dilution, and a read on the market that said ‘sell now’.

None of those are the decisions most celebrity founders make, and all of them together produced $212 million in revenue and 40% margins in 35 months.

Here’s what that was worth…

the math was actually mathing

The deal was $600 million in cash at closing, $200 million in e.l.f. Beauty stock, and a $200 million earnout tied to rhode hitting specific sales and profit targets over three years, with a total value up to $1 billion.

J.P. Morgan ran the deal for rhode, Skadden handled rhode’s legal work, and Hailey hired Cravath separately for her personal representation. The presence of J.P. Morgan, Skadden, and Cravath tells you something before you even get to the numbers.

Contrary to the Reddit reporters’ speculations, this was not a handshake deal with a press release attached.

Real quick…

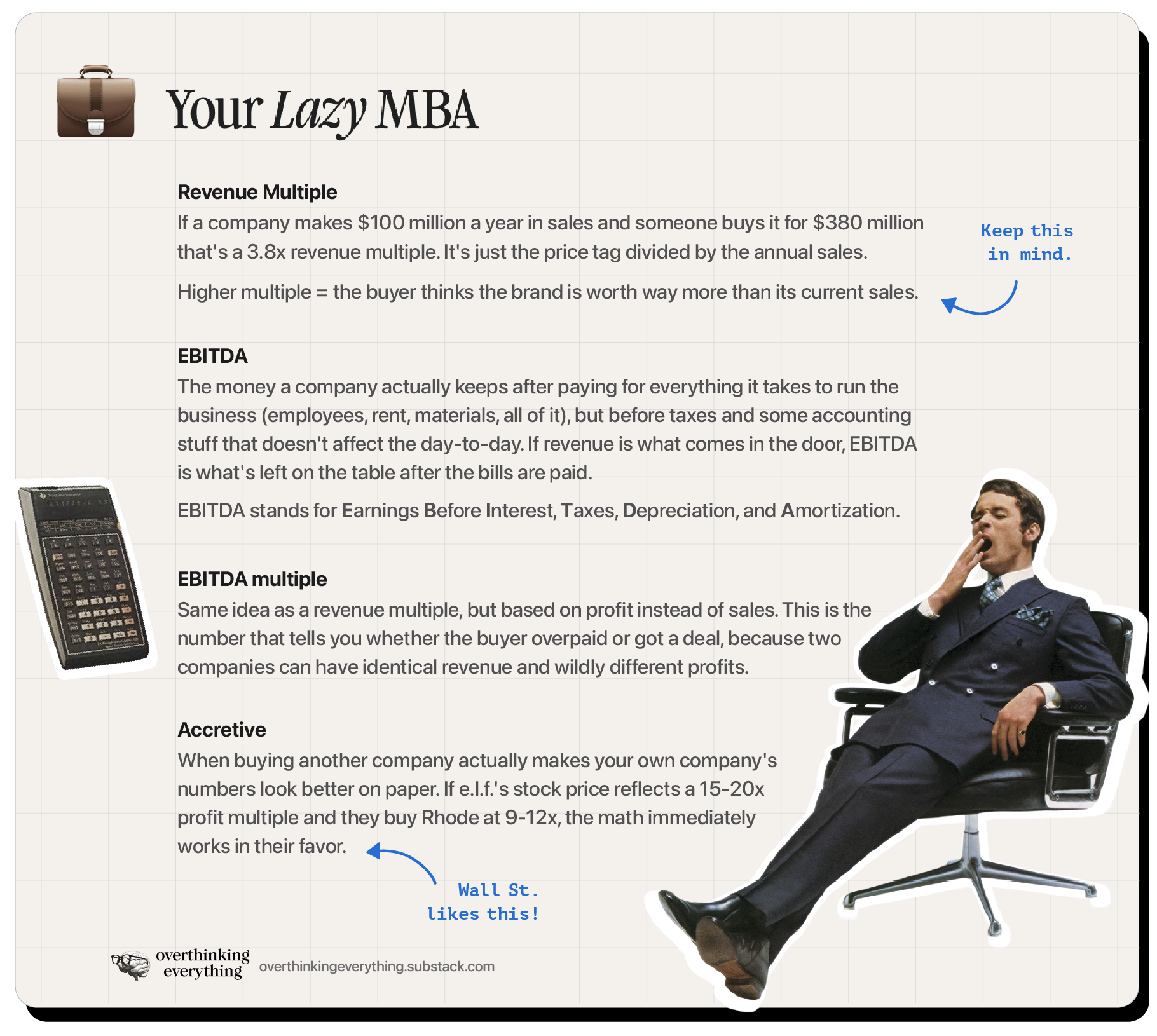

Before we head into this next rundown, I want to give a quick translation for the non-finance reader. If you’re up to your ears in MBA tuition debt and already know this stuff, you may Pass Go and read on…

Ok, now where were we…

Ah yes. At the time of the acquisition, rhode was doing $212 million in annual revenue with 40% margins.

That single sentence is one we need to suss out a bit.

It means rhode had grown from a three-product launch in June 2022 to a $212 million business by May 2025.

In 35 months.

It also means the brand was generating roughly $84.8 million in operating profit annually, which is an unusual number for a celebrity beauty brand at that age.

For context, Kylie Cosmetics was reportedly doing $177 million in revenue when Coty bought 51% in 2019, after four years of operation, and Kylie did not have 40% margins. The profitability at rhode was as impressive as the revenue, possibly more so.

On a straight revenue multiple, the deal is less dramatic than the headline suggests. $800 million at signing divided by $212 million in revenue is roughly 3.8x. The full $1 billion is about 4.7x.

For comparison, e.l.f. bought Naturium in 2023 for $355 million when it was doing approximately $100 million in revenue, a 3.5x multiple.

rhode commanded a premium over Naturium, but not a shocking one. What the revenue multiple tells you is that e.l.f. is a disciplined acquirer that doesn’t dramatically overpay on topline.

The EBITDA multiple tells a different story. $84.8 million in operating profit against an $800 million signing price is roughly 9.4x. Against the full $1 billion it’s about 11.8x.

In early 2025, e.l.f. itself was trading at approximately 15 to 20x EBITDA. Buying rhode at 9 to 12x EBITDA while your own stock trades at a higher multiple means the acquisition was immediately accretive on paper. This is the number that made the deal rational from e.l.f.’s board’s perspective, and it appeared in exactly zero of the 207 comments in the r/MakeupAddiction thread.

The tariff theory that surfaced in the thread (and got 1.3K upvotes) is worth taking seriously. e.l.f. has historically sourced the majority of its manufacturing from China, which became a real liability as tariff escalation accelerated through 2024 and 2025.

rhode’s domestic U.S. manufacturing footprint, modest as it was, represented real strategic optionality for an acquirer trying to reduce supply chain exposure. It wasn’t the primary reason for the deal, but it wasn’t irrelevant either, and a Reddit commenter identified it before most industry analysts did. Go figure!

The thread also correctly identified that $600 million in cash was not landing in Hailey’s personal account.

🥓 How much bacon did Hailey actually bring home to The Biebs?

By the time co-founders take their share, early investors take theirs, J.P. Morgan collects its advisory fee (typically 1 to 2% of deal value, so somewhere between $8 and $16 million here), and Skadden and Cravath submit their invoices, Hailey’s personal proceeds are a fraction of the headline.

A fraction of $600 million is still generational wealth by any definition. But the estimate of roughly 25% at most for a founder’s typical equity stake in a venture-backed consumer brand is not far off the realistic math.

And Hailey isn’t done working. She retained the role of Chief Creative Officer and Head of Innovation post-acquisition, which means the $200 million earnout is partly hers to earn, and she’s still in the office. Oof!

who wants to be a billionaire?

rhode sold for roughly $1 billion because it was built like a business, not a celebrity endorsement deal.

Tight product count

Zero paid influencer spend

A hero product that generated $15 million in a single Sephora drop

Formulations that actually worked

and a founder who wore the product in every photo she posted.

e.l.f. paid for all of that simultaneously.

The question for every celebrity brand that exists right now is the same one the Reddit thread was circling without quite landing on, which is asking how much of that blueprint do you actually have, and how much of it is just a famous person with good packaging?

rare beauty (selena gomez)

Dammit, Selena..can’t Hailey have something all to herself?!

This one is an obvious enough winner that it almost feels like a spoiler.

Rare Beauty has $400M+ in annual revenue, the Soft Pinch Liquid Blush has had the same kind of organic sell-out momentum that the Peptide Lip Treatment had (the kind where customers are immediately adding to cart, not waiting for a coupon code), and the brand launched at Sephora by breaking the retailer’s single-day sales record.

Selena has said publicly that she won’t sell. But this is historically meaningless. Founders almost always say they won’t sell until someone puts a term sheet in front of them with enough zeros that it would be irrational to refuse.

The more interesting question is who’s buying and at what valuation, which at $400M+ in revenue is almost certainly north of $2 billion.

The likely acquirer is Puig, the Barcelona-based beauty conglomerate that bought Charlotte Tilbury in 2020 for a reported $1.2 billion and has since been actively building a prestige portfolio.

Shiseido is the other name worth watching. The Rare Impact Fund, which donates 1% of sales to mental health causes, is worth mentioning not for the charitable angle but for the business one. It gives the brand equity that survives founder distance, which is one of the harder things to engineer in a celebrity beauty exit.

Rare Beauty probably stays Rare Beauty even if Selena steps back from the day-to-day. That makes it a safer acquisition than most.

the outset (scarlett johansson)

Interesting, but NOT at a rhode multiple.

RetailBoss reported a 999% sales surge for The Outset in 2025, with product drops selling out nearly instantly, and described it as the brand that “mirrors rhode’s trajectory most closely.”

That framing is compelling but slightly misleading, because trajectory and architecture are two different things. rhode’s economics worked the way they did because Hailey Bieber had a TikTok and Instagram following that made customer acquisition cost essentially zero.

Hailey posted and people bought. It was that simple.

Scarlett Johansson is one of the most famous people on earth and she oozes Hollywood superstardom, but her relationship with social media is completely different. She relies on traditional press, brand associations, and the general awareness of being a major film star. That’s just not the same as Hailey’s direct owned audience that converted to sales with no go-between.

And that changes the margin profile significantly. A brand with high customer acquisition cost and high revenue growth is a very different acquisition target than a brand with near-zero acquisition cost and high revenue growth.

The Outset is a real business with real momentum that’s worth keeping an eye on, and the clean beauty positioning is credible, but a buyer looking to replicate what e.l.f. got with rhode is going to look at the unit economics carefully and probably come in at a more conservative multiple.

huda beauty (huda kattan)

Super impressive, but not anytime soon.

Huda Beauty does over $500 million in reported annual revenue and Huda Kattan has rejected multiple acquisition offers over the years, which is either principled independence or a sign that the price hasn’t been right yet (I’m guessing it’s probably both).

The problem for anyone trying to buy it right now is that this is no longer a focused beauty brand. It seems to have morphed into a multi-category portfolio that includes Kayali fragrance and a skincare line, which means any acquirer is buying a significantly more complicated business than rhode was.

Huda is also still the content engine for the brand in a way that Hailey had begun deliberately stepping back from before the e.l.f. deal closed.

You can acquire a brand that’s ready to operate without its founder, but you can’t easily acquire one where the founder is still appearing in multiple posts a day and the whole thing runs on her personality. Skip for now.

reale actives (alix earle)

Too early to tell, but she’s definitely off to the races…even with a few stumbles at the starting gate.

For months, a secret Instagram account called “wtfisalixdoing” was running up 500,000 followers without ever explaining itself. And then there was a puzzle-piece billboard in New York and unlabeled products kept appearing in GRWM videos without any comments.

If you follow Alix Earle, you know her 14 million TikTok followers treat her like they’re in a group chat, and not like they’re on a fan page.

They had been trying to decode what was coming for weeks before she told them anything, and when she finally launched Reale Actives on March 31st, the brand hit $1 million in sales in less than five minutes and sold out its entire inventory by 4pm.

For an acne brand. On a Tuesday. That’s some crazy work.

But Alix’s four-product lineup also launched into immediate controversy. The campaign showed Earle with entirely clear skin, and the internet noted she has been on three rounds of Accutane and currently takes 100mg of spironolactone daily.

The TikTok jury of her non-peers decided this disqualified her from the acne space entirely.

But Alix posted a response and kept it cute.

“I’m not here to lie, I’m not here to try and trick anyone. If you believe me, you believe me. If you don’t, whatever.”

This is, if you squint, basically the same energy rhode had when TikTok called the Peptide Lip Treatment overpriced and it sold out anyway.

The question acquirers are going to ask is not whether Alix Earle should be selling skincare. It’s whether she built this the way Hailey built rhode. The launch architecture says maybe, and maybe is more than most celebrity founders start with.

Four SKUs to rhode’s three makes this very interesting.

And Imaginary Ventures is a backer, which is the same fund that got into Glossier early and knows the difference between a real skincare business and a marketing exercise.

And Alix’s customer base of fans is ride or die. They didn’t show up because of a billboard. They had been watching the whole thing unfold for years, and when Earle said these were the products that worked for her, they believed her because she had earned their trust.

However…the gap is the hero product.

rhode became acquirable because the Peptide Lip Treatment became the thing, the product that sold out in ten minutes and generated $15 million in a single Sephora drop and gave the whole brand a name in one SKU.

Reale Actives doesn’t have a clear equivalent yet, and whether the Go Deep Mandelic Acid serum becomes that for Earle’s audience depends entirely on whether the people who bought it on launch day tell TikTok it worked.

Another point to consider is that $1 million in five minutes is a debut number, not an entire business.

rhode became worth a billion dollars because the sales didn’t stop on launch day and neither did the margins. If Reale Actives has the same reorder mechanics, the TikTok controversy is a footnote and the Imaginary Ventures call looks brilliant in hindsight.

If it doesn’t, “wtfisalixdoing” will likely turn out to have been the most interesting chapter of all of this.

Let’s check back in twelve months.

kylie cosmetics (kylie jenner)

Already over.

Coty bought 51% for $600 million in 2019 and had written the valuation down significantly by 2022.

Twenty-nine products at launch, built on wild social media fury rather than product quality, and sold before the reorder data had time to tell the real story.

Truth be told, this is the cautionary tale everyone else on this list is being measured against, and it’s the reason rhode’s tight SKU count and actual margins looked so compelling to e.l.f. by comparison.

fenty beauty (rihanna)

Nope.

Rihanna owns 50%. LVMH owns the other 50%. LVMH doesn’t sell trophy assets. There is nothing to acquire here.

I’ve been thinking way too much. It’s your turn!

What brand are you watching right now that you think is probably being built to sell? Drop it in the comments. I read all of them, and the good ones might end up in a future Overthinking piece.

🧠 so how can you be the next billionaire?

Probably not on the basis of five bulletpoints in a Substack newsletter, to be fair. rhode was built over 35 months through about a hundred small decisions that compounded on top of each other, and most of them happened before any of us were even paying any attention.

So of course I can’t give you the whole playbook. But I can give you the part of the playbook that was visible from the outside if you knew what to look for, which is the part worth stealing. Start here.

Know your actual customer acquisition cost, not the one you think you have. Most brands spend 15 to 25% of revenue on influencer and paid marketing and treat it as a fixed operating cost, which is fine until an acquirer opens the books and asks what happens to the business if you stop. rhode's was near zero because Hailey Bieber posting about the product was the marketing channel, and she was going to keep doing it because she was the founder. If your growth requires budget to sustain it, that budget shows up in your margin profile, in your due diligence, and eventually in the multiple you command. Know the number before someone else tells it to you.

Launch fewer products than feels comfortable, and don't add more until the first one earns it. rhode launched with three SKUs and waited. Three products meant every dollar of manufacturing attention and every unit of operational complexity pointed at the same thing. It also means that when e.l.f. ran due diligence, the revenue was concentrated and easy to underwrite. A brand doing $200 million across three hero SKUs is a fundamentally different acquisition target than a brand doing $200 million spread across thirty, even if the top line looks identical.

Don't pick your hero product in advance. Let the market pick it, then move everything behind it. rhode didn't decide the Peptide Lip Treatment was going to be the thing. They launched three products and one of them sold out in ten minutes and kept doing it. The move most founders make at that point is to expand the line, build out the range, show investors there's depth. rhode left the Lip Treatment alone for two years and let it accumulate virality before expanding meaningfully around it. It generated $15 million in a single Sephora drop. Patience with a winning product is harder than it sounds and worth more than it looks.

Make sure the product works when you're not in the room. The reason rhode's formulations mattered to an acquirer is not just that customers liked them. It's that a brand whose product survives founder distance is a different risk profile than one that dissolves the moment the founder moves on. KKW Beauty essentially stopped existing when Kim Kardashian did. rhode's products could be recommended by a dermatologist who had never heard of Hailey Bieber. That’s partly why the margins came in at 40% and partly why e.l.f. felt comfortable paying $600 million in cash at closing.

Watch the category and sell while the story is still good. Hailey watched Coty buy 51% of Kylie Cosmetics for $600 million in 2019 and write it down significantly by 2022. She watched SKKN by Kim get middling reviews. The celebrity beauty window was open in May 2025, e.l.f.'s stock was near its peak, and she moved. Most founders wait because they want one more year of growth to justify a higher number. One more year of growth in a softening category often produces a lower exit than slightly less growth while the category is still hot. Pay attention to timing. It matters so much more than you might think.

what happens to rhode from here

Now don’t be fooled. Things aren’t all sunshine and puppies over at rhode. A quick tiptoe into the dark web (aka r/HaileyBaldwinSnark) reveals the Glazing Milk is having a rough time.

Starting April 20th, the mini dropped from 2.2oz to 1.7oz. The large already went from 4.7 fl oz to 4.2 fl oz on the sly and picked up a $2 price increase on the way. rhode says it’s about ingredient and shipping costs. Fine, probably true.

But “accessible luxury built on founder trust” is a harder thing to maintain when the bottle is shrinking and the parent company’s CFO is publicly saying tariffs are a reason to use pricing as a lever. e.l.f. said that in May 2025, about two weeks after the deal closed.

rhode customers are now doing the math on that, in Reddit threads, with screenshots. This could be a problem…

Speaking of people doing math on brands they used to trust, I spent a frankly unreasonable amount of time thinking about why we pay $47 for a bottle of hand soap and whether any of us should feel good about it.

That piece involves a pair of 1930s French scissors that I became emotionally attached to, which I realize doesn't sound related but it is. Check this article out next if you want to keep going (and yes, you should. Don’t overthink this).